USD/JPY Price Forecast: Corrects further below 20-day EMA as Iran conflicts de-escalate

- USD/JPY extends its decline to near 158.30 as falling oil prices strengthen the Japanese Yen.

- Oil prices have declined significantly amid the de-escalation of Middle East conflicts.

- Investors await the US ADP Employment Change and the ISM Manufacturing PMI data.

The USD/JPY pair extends its losing streak for the third trading day on Wednesday, trading 0.26% lower to near 158.30 during the European session. The pair faces selling pressure as a steep correction in the Oil price due to intensified hopes of a ceasefire in the Middle East has improved the appeal of currencies, like the Japanese Yen (JPY), whose respective economies rely heavily on oil imports to meet their energy needs.

The hopes of the Mideast war ceasefire have improved as Iranian President Masoud Pezeshkian told European Union (EU) Council President António Costa on Tuesday that his country is ready to end the war with the US. However, he clarified that Tehran will end conflicts only if the United States (US) guarantees no repetitive aggression.

Meanwhile, a further correction in the US Dollar (USD) due to diminished demand for safe-haven assets in the wake of ceasefire hopes has also weighed on the USD/JPY pair. As of writing, the US Dollar Index (DXY), which tracks the Greenback’s value against six major currencies, trades 0.3% lower to near 99.50.

On the macro front, investors await the US ADP Employment Change and the ISM Manufacturing PMI data for March, which will be published during the North American session.

USD/JPY technical analysis

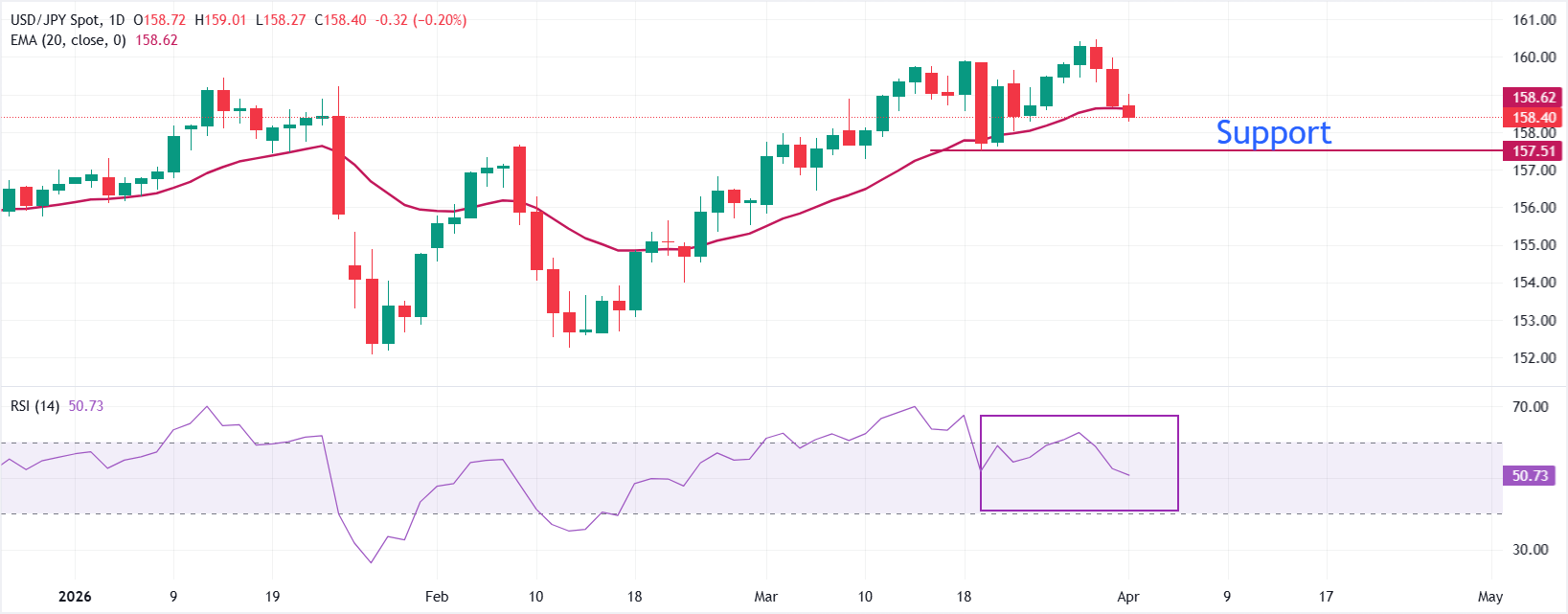

USD/JPY trades lower at around 158.40 as of writing. The near-term bias turns neutral with a mild bearish tilt as the pair slips below the rising 20-day Exponential Moving Average (EMA), hinting at a loss of bullish momentum after last week’s push above 160.00. Price now fluctuates just below the 20-day EMA near 158.60, with repeated failures to extend gains reinforcing a stalling advance.

The 14-day Relative Strength Index (RSI) retreats to near 50.00 from overbought territory seen above 69, signaling fading upside pressure rather than outright trend reversal.

Immediate resistance emerges at 159.00, where recent intraday rebounds stalled, followed by 159.80 and the 160.40 region, which capped the latest upswing. A sustained break above 160.40 would revive the bullish trend and open scope toward fresh cycle highs. On the downside, initial support is at the March 19 low of 157.50, with a daily close below exposing the February 25 high at 156.82 as the next level.

(The technical analysis of this story was written with the help of an AI tool.)

Risk sentiment FAQs

In the world of financial jargon the two widely used terms “risk-on” and “risk off'' refer to the level of risk that investors are willing to stomach during the period referenced. In a “risk-on” market, investors are optimistic about the future and more willing to buy risky assets. In a “risk-off” market investors start to ‘play it safe’ because they are worried about the future, and therefore buy less risky assets that are more certain of bringing a return, even if it is relatively modest.

Typically, during periods of “risk-on”, stock markets will rise, most commodities – except Gold – will also gain in value, since they benefit from a positive growth outlook. The currencies of nations that are heavy commodity exporters strengthen because of increased demand, and Cryptocurrencies rise. In a “risk-off” market, Bonds go up – especially major government Bonds – Gold shines, and safe-haven currencies such as the Japanese Yen, Swiss Franc and US Dollar all benefit.

The Australian Dollar (AUD), the Canadian Dollar (CAD), the New Zealand Dollar (NZD) and minor FX like the Ruble (RUB) and the South African Rand (ZAR), all tend to rise in markets that are “risk-on”. This is because the economies of these currencies are heavily reliant on commodity exports for growth, and commodities tend to rise in price during risk-on periods. This is because investors foresee greater demand for raw materials in the future due to heightened economic activity.

The major currencies that tend to rise during periods of “risk-off” are the US Dollar (USD), the Japanese Yen (JPY) and the Swiss Franc (CHF). The US Dollar, because it is the world’s reserve currency, and because in times of crisis investors buy US government debt, which is seen as safe because the largest economy in the world is unlikely to default. The Yen, from increased demand for Japanese government bonds, because a high proportion are held by domestic investors who are unlikely to dump them – even in a crisis. The Swiss Franc, because strict Swiss banking laws offer investors enhanced capital protection.